Roof Leasehold Improvements Qualified

What Is Qualified Leasehold Improvement Property

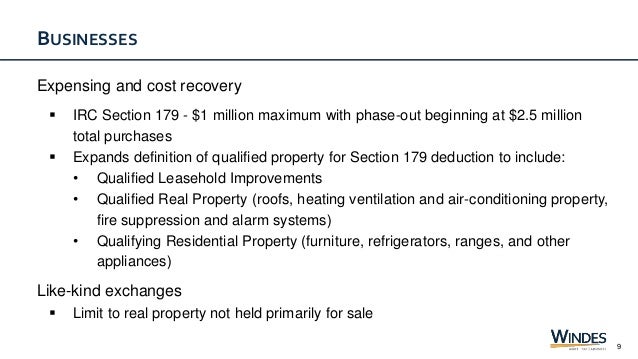

Section 179 Expensing What You Need To Know For The 2019 Tax Year Cherry Bekaert

Child Care Centres For Sale Freehold New England Region Nsw Childcare Center Childcare Business Indoor Play Areas

Depreciation Rules For Qualified Leasehold Improvements

Basement Renovations Basement Wall Paneling Ideas Budget Friendly Basement Remodeling Ideas Cheap Basement Remodel Remodel Diy Budget Basement Remodel Diy

Cares Act And Qualified Improvement Property Freed Maxick

As accounting professionals navigate the transition between asc 840 and asc 842 leases and consider the changes implemented in the tax cut and jobs act tcja of 2017 and the coronavirus aid relief and economic security act cares act enacted in march 2020 questions regarding the definitions of lease related terms and proper accounting application are in no short supply.

Roof leasehold improvements qualified.

Understanding Qualified Improvement Property Depreciation Changes Mlr

Tax Rules For Leasehold Improvements Bader Martin

Cares Act Changes The Tax Rules For Qip Depreciation Bader Martin

Irs Issues Guidance For Change To Real Property Depreciation Grant Thornton

Section 179 Tax Deduction For Commercial Buildings Cleveland Ohio Commercial Roofing Contractor

Tax Reform Mostly Increases Depreciation Opportunities For Mcdonald S Franchisees

Ex 10 17

What Is The Depreciation Of The Roof On A Commercial Building

Tax Reform Changes To Qualified Improvement Property Kbkg

Hvac Installation Qualified Leasehold Improvement Virginia Cpa Firm

Creating Permanently Affordable Owner Occupied Housing With Community

Https Dlnr Hawaii Gov Wp Content Uploads 2019 08 D 1 Ocr Pdf

Https Betterbuildingssolutioncenter Energy Gov Sites Default Files Attachments Retail Rtu Lease Language Pdf

Https Louisvilleky Gov File Daretocareleasepdf

Exhibit

Kbkg Tax Insight Qualified Improvement Property Qip Technical Correction In Cares Act Kbkg

4 Things To Know About Tenant Improvement Allowances

The Life Of The Bill June 2016 September 27 2017 November 16 Ppt Download

Https Docs Legis Wisconsin Gov Raw Cid 1087164

Kbkg Tax Insight Qualified Improvement Property Qip Technical Correction In Cares Act Kbkg

Think Tax Reform Won T Impact Your Business Think Again Rob Hende

How Bonus Depreciation Affects Rental Properties Millionacres

New Tax Law Affects Rental Real Estate Owners Pugh Cpas

Https Www Mgic Com Media Value Adds Training Appraisal Training Materials 71 40263 Manual Pdf Appraisal Participant Book Pdf La En

Source : pinterest.com